For decades the politics of trade and the raw arithmetic of geology have quietly intersected in one crucial corner of the global economy: rare earth elements. Now, Beijing’s recent moves to tighten controls on rare-earth materials and related technologies have reignited a familiar and dangerous dynamic: the weaponization of supply chains.

What began as export curbs and licensing requirements risks becoming the next global tariff showdown, with ripple effects for industry, defence and the green-energy transition. China produces the bulk of the world’s processed rare earth, the 17 elements (15 lanthanides plus scandium and yttrium) essential to electric-vehicle motors, wind-turbine generators, precision-guided munitions and the permanent magnets that power consumer electronics.

In recent policy actions Beijing has expanded export restrictions and licensing requirements for rare-earth minerals, components and the equipment used to process them, moves Beijing frames as national-security safeguards. Reuters reported Beijing’s package of export limits introduced in 2025 as a response to U.S. trade measures, explicitly targeting supply of minerals and downstream materials.

Those moves came on the heels of broader October 2025 measures that tightened controls on rare-earth products, specialist refining equipment and technologies used in magnet manufacture; some restrictions were slated to take effect December 1, 2025.

Awaiting Another Wave of Tariffs War

Independent analysts and international agencies warned that, if enforced, such measures would tighten global supply and increase price volatility for critical inputs used across high-tech and defence supply chains. The International Energy Agency (IEA) has noted that export controls of this kind materially raise concentration risks for low-carbon technologies that rely on rare-earth magnets.

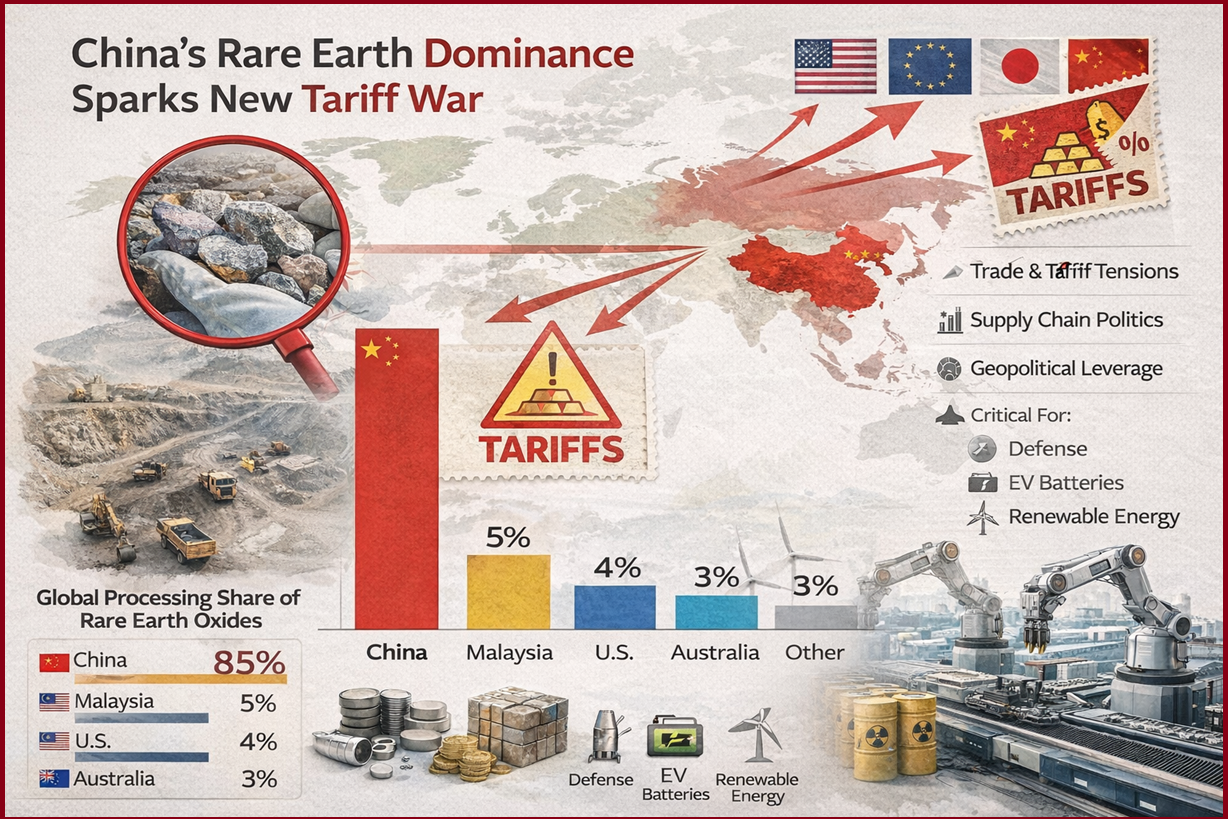

The supply-side concentration is striking. Public datasets and assessments by geological services show China dominates processing even when measured separately from raw mining. The U.S. Geological Survey (USGS), the most widely cited public source on mineral production and trade, reports that China accounts for the overwhelming share of refined rare-earth oxides and permanent-magnet production.

U.S. imports are modest in value but strategically concentrated in a handful of elements and alloys used in defence and green tech. The 2024/2025 USGS mineral commodity summaries remain the authoritative baseline for those figures.

In fact, a decade ago the European Union, the United States and Japan challenged China at the World Trade Organization, accusing it of export restraints that violated WTO rules. The WTO’s dispute panels and the Appellate Body found in favour of the complainants, concluding that China’s quotas and duties on rare earths, tungsten and molybdenum were inconsistent with WTO obligations.

The precedent also serves as a legal pathway for countries harmed by modern controls to seek redress, but WTO remedies are slow, resembling the World Health Organization’s stand during the Corona Pandemic.

Beyond Export Bans, Tariffs War Likely Next

Export controls are powerful because they restrict supply at source. But when an important supplier tightens the tap, importers have historically used tariffs and other trade barriers as countermeasures or to protect nascent domestic industries.

Tariffs can be both political signalling and practical protection. In prior episodes, for instance, where critical commodities or inputs have been constrained, importing states have responded by imposing counter-tariffs, subsidizing domestic processing facilities, or enacting secondary measures that effectively tax or block certain imports.

If China’s controls persist or are perceived as arbitrageable only by politically aligned partners, we should expect three linked responses from major economies:

-

Counter-tariffs and export restrictions of their own on dual-use technologies tied to China’s strategic sectors;

-

Targeted sanctions or licensing regimes aimed at Chinese firms or technologies that rely heavily on Chinese rare-earth inputs; and

-

Industrial subsidies and procurement rules to accelerate domestic processing capacity, often accompanied by temporary tariff protections to nurture that capacity.

Those policy tools are already visible in the U.S. and allied playbook, including Project Vault, a U.S. program to build strategic mineral reserves and incentives for domestic refining capacity. Recent diplomatic overtures, for example, allied coordination on critical-minerals supply, which indicate a willingness to couple industrial policy with trade measures.

The economics are simple but severe: when physical availability is uncertain, prices spike and buyers scramble, which disrupts manufacturing plans across sectors. In 2010–2012, when China’s export restrictions first tightened, prices for certain rare-earth oxides surged and supply chains reoriented. Global manufacturers faced higher input costs, production delays and increased incentive to onshore processing, but onshoring is expensive, dirty and slow. A decade later the market is again testing that reality.

Companies at both ends of the chain, mining and processing, feel collateral strain. Producers outside China such as Australia’s Lynas Corporation and U.S.-listed MP Materials have seen renewed investor interest, while downstream firms, from automakers to defense contractors, face higher procurement costs and squeeze on margins.

Strategic Implications For Defence, Climate Goals

Rare earths are not just commercial inputs; they are strategic enablers. Permanent magnets are central to electric-vehicle motors and advanced radar or guidance systems. Any supply disruption complicates defence planning and the transition to low-carbon technologies. Governments therefore face a hard tradeoff: prioritize short-term economic retaliation (tariffs, countermeasures) or accelerate long-term resilience (new mines, refineries, recycling, strategic stockpiles). Many will do both.

Beijing frames its measures as defensive. China’s leadership, during recent inspections of rare-earth facilities, emphasized the element of national security and the need to protect domestic strategic capabilities. As Premier Li Qiang signalled during inspections, rare earths are “increasingly important” to industrial and defence objectives.

Western policymakers and industry leaders counter that market openness and diversification are the durable solutions. A former WTO ruling and recent IEA commentary warn that controls raise concentration risks and underscore the need for allied cooperation on supply chains and recycling.

As of now, countries and companies are busy pursuing several strategies:

-

Diversify sources: New mining projects in Australia, the U.S. and Africa — but geology and permitting timelines mean scale-up takes years.

-

Onshore processing: Expensive and environmentally fraught; requires technology, capital and stringent environmental controls.

-

Recycling or substitution: Promising but currently limited in scale and technical applicability for certain high-performance magnets.

-

Allied procurement blocs and strategic stockpiles: politically feasible and faster to deploy, but costly.

None of these is a quick fix. Even with concerted investment, the industry faces a time lag measured in years, not months, and the environmental constraints around refining rare earths, historically one reason China consolidated processing capacity, are significant.

A Global Tariff Flashpoint?

When raw-material supply becomes a geopolitical lever, tariffs and counter-measures become almost inevitable as governments seek to shield industry and assert leverage. The legal remedies at the WTO provide an option but not a rapid cure. Businesses should assume a period of elevated policy risk: higher input costs, more volatile supply chains, and increasing regulatory complexity, and plan accordingly.

China’s recent controls on rare earths are not an isolated trade technicality; they are a strategic manoeuvre with the potential to drive a new wave of tariffs, industrial subsidies and reshaped supply chains that will affect everything from smartphones to submarines.

The world can respond with legal challenges, industrial policy and strategic stockpiles, but the structural imbalance in processing capacity means that geopolitical frictions, and the economic distortions they create, are likely to persist for the foreseeable future.